Friday, December 4, 2015

Thursday, December 3, 2015

3 Real Estate Investment Tips for Choosing a Rental Property

3 Real Estate Investment Tips for Choosing a Rental Property

Those who intend to build or diversify their investment portfolios often choose to buy a real estate property because of its perceived inherent stability of this mode of investment. While it is true that investors may stand to earn a lot more by investing in the stocks of some blue chip company, the risks associated are usually greater too.

On the other hand, a house generally appreciates in value as the years go by. So those who want to play safe when making their investment decisions usually decide to go in for a piece of real estate. The key is to choose rental property that is most likely to bring you an impressive return.

Like stocks, shares, and bonds, the investor needs to be extremely careful when buying a property for real estate investment. Not all properties make sound investments and bring on a cash flow readily. Keep reading for a few pointers to help you choose the ideal real estate investment property.

Tip #1. Choose Single-Family Homes Over Condos

Some research studies have shown that single-family homes tend to be more suitable as real estate investment options than condos. This is primarily because of the kind of renters that the former tends to attract. More than 60 percent of all single-family home tenants have children and so move less often than unmarried individuals in their 20s and 30s and childless couples in the same age bracket. In fact, tenants of single-family home tenants are about 20 percent more likely to live in a house for five years or more.

Tip #2. Choose Rental Property with Location Advantages

When you choose rental property for a real estate investment, consider buying one that will attract tenants in droves and also definitely appreciate in value through the years. One way to ensure this is to buy a property that has obvious location advantages. While judging in the light of this criteria, keep in mind that proximity to a school district and a major interstate and the presence of recreational opportunities in the vicinity will make your property always be in high demand among tenants with varied needs.

What is more, these location advantages will ensure that the worth of your property won’t decline in future and you can sell it easily—to a family with school-going kids, a couple in their sunset years who want to settle in a quiet and safe community with lots of recreational opportunities nearby, or a couple who wants to stay somewhere from where it is easy to commute to their respective places of work.

Tip #3. Choose Rental Property That’s Built Right

When looking for a property to buy to add to your investment portfolio, always go in for a house that has a stable structure and a strong foundation. A sturdily-built house will save you hundreds and thousands of dollars in repair, replacement, and maintenance costs in the long run than a derelict and run-down house that is a few thousand dollars cheaper now. What is more, a sturdily-built house will also attract tenants readily; put yourself in the shoes of your potential tenants and you will get the picture.

The above pointers should help you zero in on a property that will ensure positive returns on your real estate investment by appealing to both tenants and sellers, like a well-built single-family house that is in a fantastic location. With many foreclosed properties in the market right now and low mortgage rates, NOW is the right time to plunge into the world of real estate investment.

Do you have any other tips on how to choose rental property that translates into a sound real estate investment? Let us know in the comments, and don’t forget to share this article.

Call Now

to See Rental Properties For Sale in

Heidi Buchberger RE/MAX Realty Center 262-443-2672 heidi.buchberger03@gmail.com

Tuesday, December 1, 2015

10 Really Smart Ideas about Selling a Home

10 Really Smart Ideas about Selling a Home

Selling a Home

____________________________________________________________________________

Selling a home is all about incorporating the right ideas into the home selling game plan. Everybody and everything seems to have a game plan, a strategy to get something done. Hey, we’re in Football season where it’s all about game plans. Who is your favorite? What NFL team has the best game plans? Well, selling a home requires a game plan too. Today, I’m going to talk about some really smart ideas to selling a home. Let’s cross that closing, finish line.

“ A few plays decide each football game ” – Vince Lombardi

Play out these ideas below and you’ll be sure to win the game of selling a home.

Smart Idea #1

You want to make sure that you want to sell your home and you’re not wishy washy about your decision to sell.

You need to make up your mind, be confident in your decision to sell and start the process.

Selling a home is not always an easy decision. There are a lot of factors that go into selling a home and a really huge factor are your emotions and letting go. Flashback to those countless memorable family meals or perhaps little Joey’s first bike ride down the driveway. The list of good times likely goes on and on as they’re etched in your memory. Savor those moments as they can never be taken from you, however when you’ve decided to sell your home, you must now put them aside and base your decisions to selling a home on solid home selling advice not clouded by memories.

This is a critical first step. Decision to sell made. Do what it takes to sell. Save yourself the agony.

Smart Idea #2

Realize that little things do matter.

It’s true! A shiny new Kitchen sink. A new Kitchen faucet. How about new knobs on your Kitchen cabinets? What could you do in your home’s Kitchen? Repair those things around your home that you’ve been meaning to do. All of these little things matter because they can make the difference in how appealing your home may be to a prospective home Buyer. And, because they’re “little” they won’t necessarily break the budget, yet will take you closer to selling your home. The costs associated with these things can amount to getting a Buyer interested for a lot less money than what you would potentially give up in price due to your home being seen as less than desirable.

Little things are key when you want big things to happen.

Smart Idea #3

Consider a Pre-Listing home inspection.

Know before you sell.

Be prepared on what a Buyer’s home Inspection would reveal. Taking care of needed home repairs will always save you money before a Buyer comes to you and tells you what repairs are needed. If a Buyer’s home Inspector’s repair estimate is between $300-$500, what estimate do you think the Buyer will use when requesting money from you in order to make the repair? Yes, you guessed it, they’ll estimate it high at $500; you immediately lost $200! Don’t let them haggle with you, take care of it before when you’ve completed your own home inspection. Or if you don’t want to take care of the items highlighted in your home Inspector’s reveal, then simply note the items on your Seller’s Property Disclosure and price accordingly so any home Buyers know what needs fixing and therefore has been reflected in the price of your home’s selling price.

Makes you ready for the Buyer’s attempt to reduce your home’s sale price.

Smart Idea #4

Trust who you hire to sell your home.

Oh, does it ever matter! Ask the right questions. Hire the right Realtor. Do your research to find out more about the Realtor you’re considering hiring. How long have they been selling homes? How long does it take them to sell a home: in other words, how fast do they sell homes? What have their customers said about them? How do the Realtors demonstrate their knowledge? Can you read Real Estate articles where they advise home Sellers how to get their home sold? Reading published content from a Realtor can be very revealing as to their trustworthiness. Trust is a must and if you don’t trust your current Realtor, time to find a new one.

Delivering on Real Estate promises are essential.

Smart Idea #5

Price your home based upon fair market value and not upon how you feel about your home.

Buyers will only pay fair market value for your home. Buyers do not have the emotional attachment that you have in your home, therefore you cannot attach any market value to such a feeling. There are practical and sound ways in which to price a home for sale that your Realtor will employ to get your home sold. Your Realtor should be skilled at pricing homes to sell. Simply listing your home for sale higher than market value will have it languishing on the market for weeks and months on end, only to further devalue your home with price reductions needed. Don’t be a statistic where home Sellers chase the market. Price it right at the onset! There are ways and methods in which to value a home and unfortunately, feelings don’t factor in.

Through your Realtor’s reason you’d be wise to control your emotions to get your home sold.

Smart Idea #6

Don’t brush anything under the rug.

Hiding imperfections about your home can prove costly in time, money and even jail! Never think that you can hide any problems about your home. If you know something about your home that could affect it’s value, you need to inform your Realtor and any prospective Buyer.

Seller’s written disclosure requirements about the home they’re selling may vary by state, yet advising of what you know that may affect its value isn’t optional.

Selling a home requires that you fess up anything that you know about it, particularly if what you know may affect its value.

Plan on confessing any prior repairs or current conditions to avoid problems now or in the future after you sell your home.

Smart Idea #7

Make sure prospective Buyers are well qualified, financially, to buy your home.

Find out your Realtor’s method to assure this.

Nothing is worse than accepting a Buyer’s offer to buy your home only to later find out they can’t qualify to secure a mortgage.

Any prospective home Buyer should have gone through a detailed mortgage Pre-Approval process that enables them to convey confidence in the ability to buy your home.

Get it in writing. Get all the details of their financial ability. Don’t accept a casual conversation had with their Lender.

Smart Idea #8

Be well informed about the home selling process.

Get educated. Understand. Anticipate. And know what to expect.

It’s important to know what to anticipate when you sell a home. Knowing what to expect will result in a much smoother process with a better home selling outcome.

From initial preparation, to home showings, to the Buyer’s offer, their inspections, appraisals and getting to the closing table, it’s best to be in the know. Your Realtor will advise you on what to expect.

Reduce your level of anxiety by understanding the home selling process.

Smart Idea #9

Make your home sparkle before it hits the market for sale.

Sparkle can immediately generate Buyer interest and higher dollar. Don’t open up the curtains to your home until your home has been thoroughly prepared in anticipation and expectation of genuine Buyer interest.

Sparkle usually doesn’t entail huge sums of money, but rather huge determination, commitment and elbow grease to get your home ready to sell.

Smart Idea #10

Know that your home sale will cover your costs.

Don’t let a surprise hit you at closing where you’re asked to bring money to closing! There are a number of costs associated with selling a home and to avoid any of those nightmare closing surprises, make sure you understand up front what it is that you can expect to pay to sell a home. Your Realtor should provide you with an estimate of your closing costs that go beyond the commission that you pay to sell a home.

Get it covered when selling a home.

Finishing up in the closing end zone.

These really are smart ideas to get your home selling game plan over the finish line, don’t you think?! These will most certainly put you a position of strength.

Home selling really doesn’t have to be full of gaps. Simply put into practice these smart ideas and you’ll be on your way to handing the keys off to a happy new home Buyer and cross over into the closing end zone.

Monday, November 30, 2015

How to Get Mortgage Loan Paperwork Right the First Time

How to Get Mortgage Loan Paperwork Right the First Time

There is no getting around the paperwork involved in applying for a mortgage loan.

Mortgage lending qualifications have tightened in a post-recession world—meaning whether you’re applying for a government-backed loan, a qualified mortgage loan or even a jumbo loan, you’ll face more paperwork than ever before.

Fail to turn in some of the required documents, and you could get turned down.

Your lender may require more or less, but here are the general guidelines to help you prepare.

Show How You’ll Use the Mortgage Loan

Before a lender will approve your mortgage loan, they need to know what you’re borrowing the money for and how you’ll manage the expenses that come with the property. You might need to show this information:

- Information about the property in question

- Your purpose in getting the loan

- Present and proposed housing expenses

- Copy of contract if it is a purchase

- Copy of current mortgage statement if refinancing

Much of this information is a matter of public record, and both your REALTOR® (Heidi Buchberger RE/MAX Realty Center) and your lender can help you gather what you need.

Personal Information

In addition to verifying why you’re asking for a mortgage loan, a lender will also verify you are who you say you are. This means providing a personal identification documents such as the following:

- Often two forms of government identification, such as a passport and driver’s license

- Social Security number

- Copy of divorce decree if you are divorced

- Legal status, legal problems or other financial obligations that would not appear on the credit report

Income and Assets

Your lender will want to know about your income and assets. Presenting a complete picture of your net worth can increase your chances of getting approved for a loan. Start gathering the documentation below.

Income verification:

- Proof of income for each borrower on application—two years of W2 forms or paystubs, if you are a wage earner

- Two years of tax returns (with all schedules)

- Year-to-date profit and loss statement if you are self-employed

- Documents about other possible sources of income such as child support, Social Security or alimony

Assets:

- Proof of assets for each borrower on application — two or three months of bank statements for all assets, with all pages of the statement

- Explanations of any bank accounts opened in the last six months

- Letter of explanation and a source for any money given to you as a gift

Credit, Borrowing History and Debt

If you’re shopping for a qualified mortgage, you’ll face tight income-to-debt ratio requirements. Under the Dodd-Frank Act, a borrower can have no more than a 43% debt-to-income ratio, and lenders are required to verify your income—and check your credit to make sure you qualify under these terms.

Be prepared to supply a lot of this information about your borrowing history and debts:

- Credit report disclosure form—a document allowing the lender to pull a copies of your credit reports and credit scores

- Information about bankruptcies—including a copy of petition and discharge, a written explanation of what happened to cause the bankruptcy, and how your situation has changed

- Information on any other properties owned and what current debts you hold

- Letter from your current or previous landlord showing positive rental history

Keep in mind, whenever you send anything to a lender, it is important to present it in an easy-to-understand way. Be as brief as you can in your explanations.

Also, your paperwork must present a complete picture, one that cannot be open to misunderstandings by an overworked underwriter on the other side.

If you approach the mortgage loan application process the right way, you will be more apt to provide the lender what they need, making it a smooth process.

Saturday, November 28, 2015

8 Benefits of Buying a House at Year’s End

8 Benefits of Buying a House at Year's End

Summer may be real estate’s busy season, but winter offers great opportunities for buying a house, especially for renters looking to become homeowners, growing families trading up to larger houses and baby boomers seeking homes to fit their evolving lifestyles.

Generally speaking, your housing choices during the late fall are still healthy. October and November are great months to go house hunting. December is usually sparse, market-wise, but if that fits your timeline, you could luck out.

The benefits to buying a house at the end of the year include the following:

1. Tax savings

If you close by December 31, you can deduct mortgage interest, property taxes, points on your loan and interest costs. These deductions are significant, especially in the early years of your loan when you’re paying off a lot of interest.

2. Motivated sellers

Many sellers want to enjoy tax savings on the next home they purchase. They may accept lower bids in order to meet Uncle Sam’s deadlines. However, if you’re in a strong seller’s market, you’ll want to be conservative and heed advice from your real estate professional.

3. Builder incentives

If you’re buying a house that is brand new, there’s a good chance builders may push to close the books on their year—and meet quotas. They may offer upgrades or little extras to sell houses before the calendar turns.

4. Available movers

Many moving companies are booked six weeks or more in advance during the busy summer months. In the fall and winter, it’s normally easier to secure the services of a moving company or rental equipment on shorter notice.

5. Paying toward something you own

If you’re renting, your monthly check goes toward something that will last you a month: You’ll never see any return on that money. When you buy a house, your monthly mortgage payment goes toward an investment—and ultimately a roof that’s yours.

6. Consistent payments

Landlords can increase your rent. Once you secure a mortgage, you can rely on consistent payments if you have a fixed-rate loan.

7. Freedom to renovate

Modernize your kitchen, paint your home’s exterior neon orange, change your fixtures or replace your carpeting; whatever inspires you, no one can tell you, “No!”

8. Gaining equity

In the beginning, most of your payment goes toward interest. But gradually more will go toward paying off your principal, meaning you build up equity—or savings—in your home. Another factor in equity is appreciation: As home values rise, so does your rate of equity.

Updated from an earlier version by Michele Dawson.

Thursday, November 26, 2015

Tuesday, November 24, 2015

Home Equity Matters...Build Your Wealth

Home Equity Matters A LOT…

There are many reasons, both financial and non-financial, that home ownership remains an important part of the American Dream. One of the biggest reasons is the fact that it helps build family wealth. Recently, Freddie Mac wrote about the power of home equity. They explained:

“In the simplest terms, equity is the difference between how much your home is worth and how much you owe on your mortgage. You build equity by paying down your mortgage over time and through your home's appreciation. In a nutshell, your money is working for you and contributing toward your financial future.”

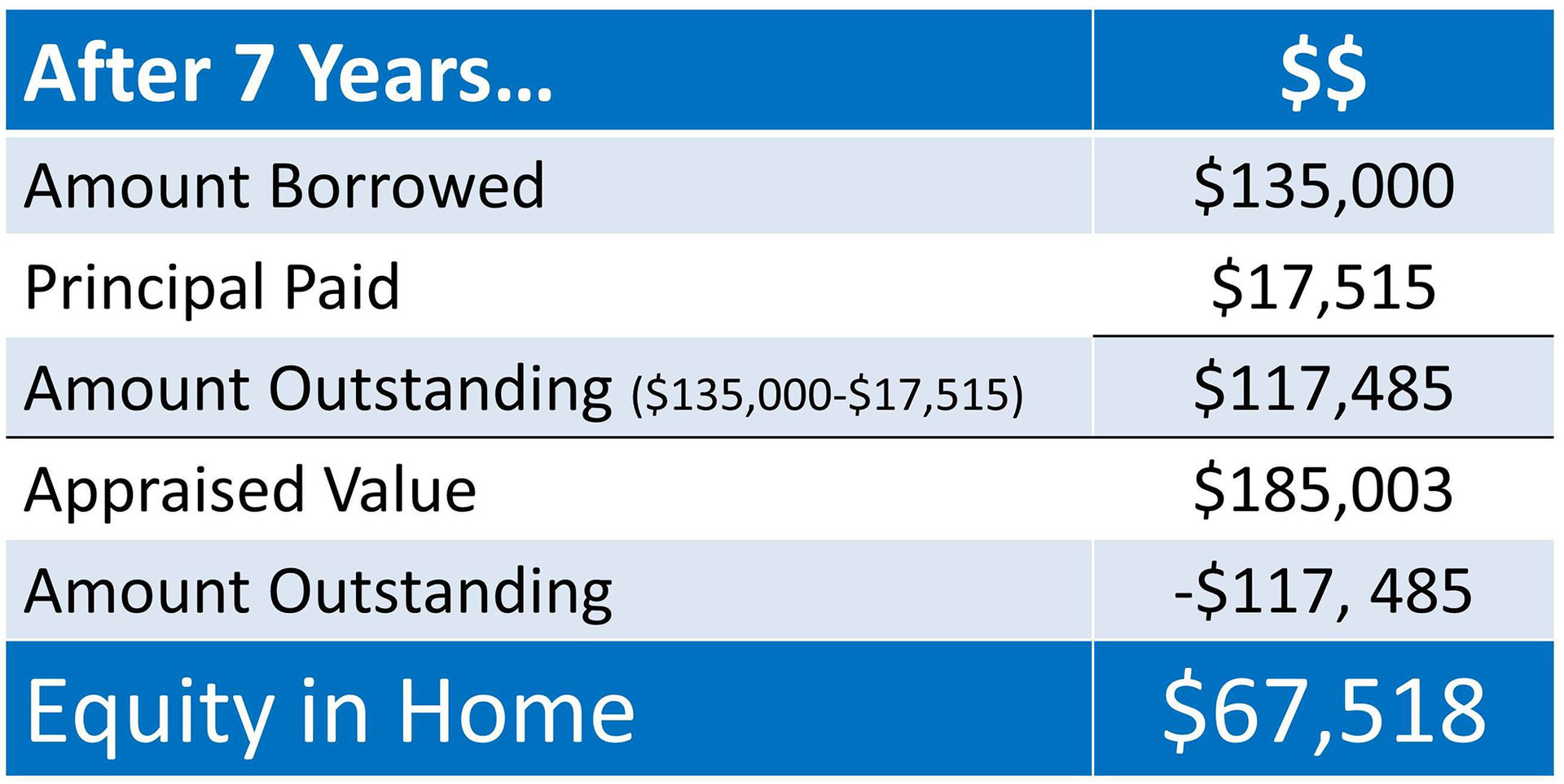

They went on to show an example where a person bought a home for $150,000 with a down payment of 10% ($15K), resulting in a loan amount of $135,000. The buyer secured a 30-year fixed-rate mortgage at 4.5% with a monthly mortgage payment of $684.03 (not including taxes and insurance).

The chart below demonstrates the home equity built after 7 years of making mortgage payments and assuming the historic national average of 3% per year home appreciation:

And that number continues to build as you continue to own the home.

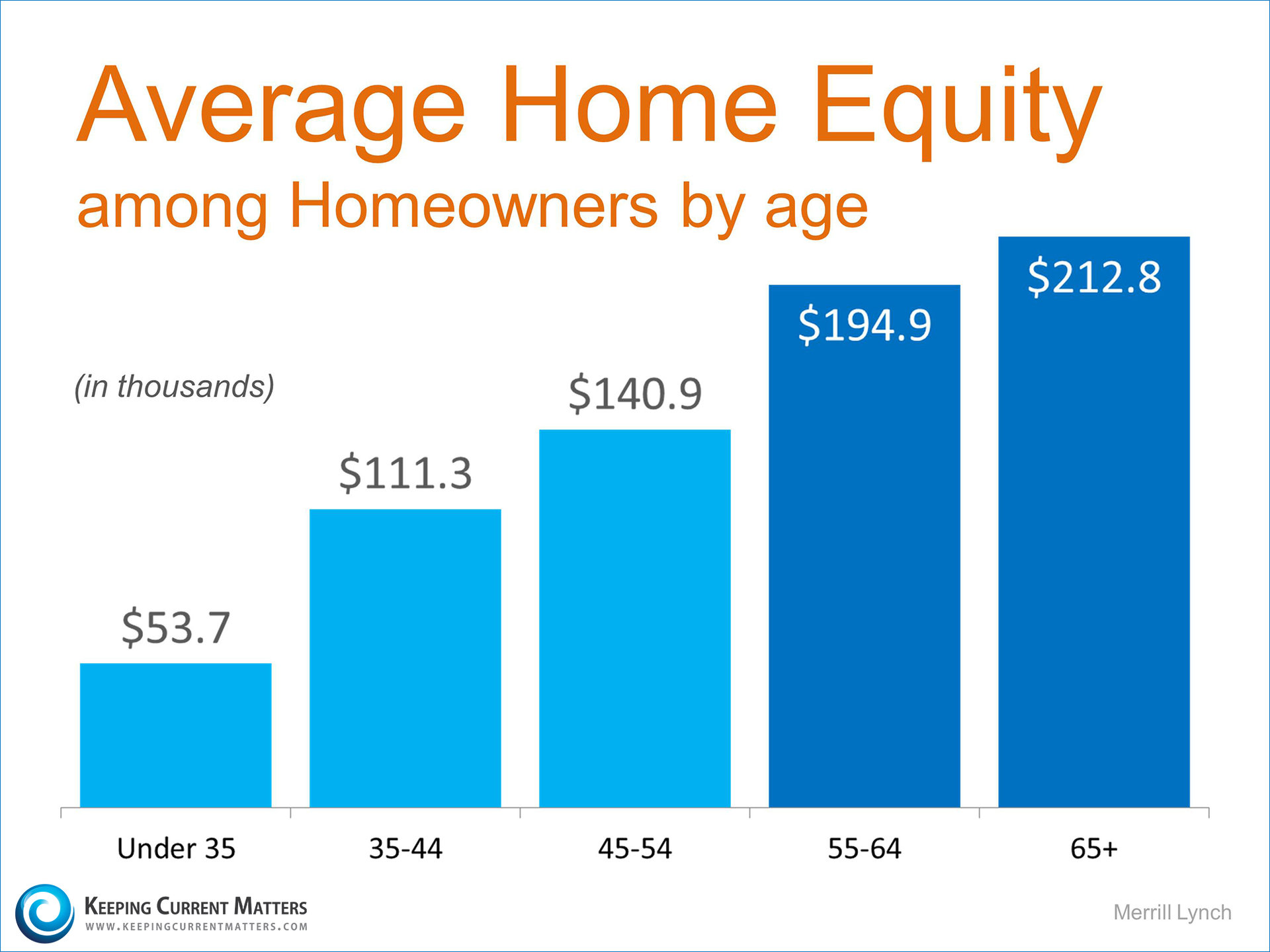

Merrill Lynch published a report earlier this year that showed the average equity homeowners have acquired by certain ages.

Bottom Line

Home equity is important to building wealth as a family. Referring to the first scenario above, Freddie Mac explained:

“Now, if you continued to rent, and made the same payment of $684.03 per month, you'd have zero equity and no means to build it. Building equity is a critical part of home ownership and can help you create financial stability.”

Put your housing cost to work for you and your family. Meet with a real estate professional today to explore your options.

Contact Heidi Buchberger RE/MAX Realty Center 262-443-2672 heidi.buchberger03@gmail.com for all your home buying and selling needs in Waukesha County, Jefferson County, and Milwaukee County.

Subscribe to:

Posts (Atom)