![Change In Home Sales By Price Range [INFOGRAPHIC] | Keeping Current Matters](https://lh3.googleusercontent.com/blogger_img_proxy/AEn0k_vu9AnVedl7f_TZG3iKPk3Kjxn-RtlFR-d-JU5sV76ujOdOcDy8ymXQML4ZItes2wPycY3_oyLJNikrJotZJqgfg8C02tO6CQNoBfCkj4NI2BoWRlD2fVeAfLSiOiqO1k0w7bytiQnCrf0Sn6Cu-X7ljA9HoZc4dohX6iqt9gGR=s0-d)

Sunday, January 31, 2016

Saturday, January 30, 2016

![Why Do Americans Consider Moving? [INFOGRAPHIC] | Keeping Current Matters](https://lh3.googleusercontent.com/blogger_img_proxy/AEn0k_tdTeVwEsMSLFRbRXPEiNxYSyjfYrnQy0U0hMWZmwQXRMChT89E5qyQpkk1OvfPJR_nRSbKoQxxGs7oQ6l-fZ5ulKH7QjQ-FZLEcX7gsUYAvKoZenmiZ4k9ggeyVcqqrAwBP8Zr7gMrNW_2mK-t8lM0vpPqyD-UT-3UfovLkA=s0-d)

Friday, January 29, 2016

Buying a Home? Know ALL Your Options

In a post earlier this week, we suggested that the Millennial generation’s struggles with student debt and the overarching concept of homeownership are not the reasons for so many first time buyers hesitating to move forward with the purchase of their first home. Now there is another firm suggesting the same. The asset management company,Nomura, came out with strong guidance to their investors. According to an article inHousing Wire last week:

“Nomura’s note to clients has a take few have offered: The first time homebuyers are holding out and it’s not student debt, a shift away from homeownership as a choice by Millennials, or any of that.”

Instead, they think it is a lack of a full understanding of the mortgage process. The article explains:

“Analysts say it’s not that Millennials and other potential homebuyers aren’t qualified in terms of their credit scores or in how much they have saved for their down payment.It’s that they think they’re not qualified or they think that they don’t have a big enough down payment.” (emphasis added)

This comes off the heels of a survey by Zelman & Associates that revealed that 38% of those between the ages of 25-29 years old and 42% of those between the ages of 30-34 years old believe that a minimum of 15% is required as a down payment to purchase a home. In actually, a purchaser may be able to put down far less.

The Reality of the Situation

According to Christina Boyle, Freddie Mac’s VP and Head of Single-Family Sales & Relationship Management, in a recent Executive Perspectives piece:

- A person “can get a conforming, conventional mortgage with a down payment of as little as 5 percent (sometimes with as little as 3 percent coming out of their own pockets)”.

- Freddie Mac's purchase of mortgages with down payments under 10 percent more than quadrupled between 2009 and 2013.

- More than one in five borrowers who took out conforming, conventional mortgages in 2014 put down 10 percent or less.

- Qualified borrowers can further reduce the down payment coming out of their own pockets to 3 percent by lining up gifts from family or grants or loans from non-profits or public agencies.

Ms. Boyle goes on to explain:

“Letting more consumers know how down payments are determined could bring more qualified borrowers off the sidelines. Depending on their credit history and other factors, many borrowers can expect to make a down payment of about 5 or 10 percent.”

Bottom Line

If you have considered purchasing a house or moving-up to a new dream home, know all of your options. Reach out to a real estate and/or mortgage professional in your marketplace to get the best, most up-to-date information available. You may be surprised to learn what you and your family are capable of achieving.

Thursday, January 28, 2016

5 Financial Reasons To Buy A Home

We have reported many times that the American Dream of homeownership is alive and well. The personal reasons to own differ for each buyer, with many basic similarities.

Eric Belsky, the Managing Director of the Joint Center of Housing Studies at Harvard University expanded on the top 5 financial benefits of homeownership in his paper -The Dream Lives On: the Future of Homeownership in America.

Here are the five reasons, each followed by an excerpt from the study:

1.) Housing is typically the one leveraged investment available.

“Few households are interested in borrowing money to buy stocks and bonds and few lenders are willing to lend them the money. As a result, homeownership allows households to amplify any appreciation on the value of their homes by a leverage factor. Even a hefty 20 percent down payment results in a leverage factor of five so that every percentage point rise in the value of the home is a 5 percent return on their equity. With many buyers putting 10 percent or less down, their leverage factor is 10 or more.”

2.) You're paying for housing whether you own or rent.

“Homeowners pay debt service to pay down their own principal while households that rent pay down the principal of a landlord.”

3.) Owning is usually a form of “forced savings”.

“Since many people have trouble saving and have to make a housing payment one way or the other, owning a home can overcome people’s tendency to defer savings to another day.”

4.) There are substantial tax benefits to owning.

“Homeowners are able to deduct mortgage interest and property taxes from income...On top of all this, capital gains up to $250,000 are excluded from income for single filers and up to $500,000 for married couples if they sell their homes for a gain.”

5.) Owning is a hedge against inflation.

“Housing costs and rents have tended over most time periods to go up at or higher than the rate of inflation, making owning an attractive proposition.”

Bottom Line

We realize that homeownership makes sense for many Americans for an assortment of social and family reasons. It also makes sense financially. If you are considering a purchase this year, contact a local professional who can help evaluate your ability to do so

Wednesday, January 27, 2016

Rents Still Skyrocketing

Zillow recently revealed that the 43 million renter households in the US spent $535 billion on rent in 2015. Aggregate numbers like these often make it difficult to truly assess a situation. For more clarity, we want to share some points that were made in aWall Street Journal article earlier this month.

The article made two important points:

1. Rents are increasing faster than the last several years:

“Apartment rents increased faster last year than at any time since 2007.”

2. Rent increases are accelerating

“Another report from Axiometrics Inc., a Dallas-based apartment research company, showed that rents increased 4.7% in the fourth quarter compared with the same quarter a year earlier, the strongest year-end performance since 2005”.

Here is a graph to illustrate the rate of increase over the last several years:

Tuesday, January 26, 2016

FSBO, List Again- A Sellers Dilemma

At the end of December, in every region of the country, hundreds of homeowners have a tough decision to make. The ‘listing for sale agreement’ on their house is about to expire and they now must decide to either take their house off the market (OTM), For Sale by Owner (FSBO) or list it again with the same agent or a different agent.

Let’s assume you or someone you know is in this situation and take a closer look at each possibility:

Taking Your Home off the Market

In all probability, after putting your house on the market and seeing it not sell, you’re going to be upset. You may be thinking that no one in the marketplace thought the house was worthy of the sales price.

Because you are upset, you may start to rationalize that selling wasn’t that important after all and say,

“Well, we didn’t really want to sell the house anyway. This idea of making a move right now probably doesn’t make sense.”

Don’t rationalize your dreams away. Instead, consider the reasons you decided to sell in the first place. Ask your family this simple question:

“What made us originally put our home up for sale?”

If that reason made sense a few months ago when you originally listed the house, chances are it still makes sense now. Don’t give up on what your family hoped to accomplish or on goals your family hoped to attain.

Just because the house didn’t sell during the last listing contract doesn’t mean the house will never sell or that it shouldn’t be sold.

Re-Listing with your Existing Agent

For whatever reason, your house did not sell. Perhaps you now realize how difficult selling a house may be or that the listing price was too high, or perhaps you’re now acknowledging that you didn’t exactly listen to your agent’s advice.

If that is the case, you may want to give your existing agent a second chance. That’s a perfectly okay thing to do.

However, if your agent didn’t perform to the standard they promised when they listed your home you may want to either FSBO or try a different agent.

For Sale by Owner

You may now believe that listing your house with an agent is useless because your original agent didn’t accomplish the goal of selling the house. Trying to sell the house on your own this time may be alluring. You may think you will be in control and save on the commission.

But, is that true? Will you be able to negotiate each of the elements that make up a real estate transaction? Are you capable of putting together a comprehensive marketing plan? Do people who FSBO actually ‘net’ more money?

If you are thinking about FSBOing, take the time to first read: 5 Reasons You Shouldn’t For Sale by Owner.

List with a New Agent

After failing to sell your home, you may no longer trust your agent or what they say. However, don’t paint all real estate professionals with that same brush. Have you ever gotten a bad haircut before? Of course! Did you stop getting your hair cut or did you simply change hair stylists?

There is good and bad in every profession—good and bad hair stylists, agents, teachers, lawyers, doctors, police officers, etc. And just because there are good and bad in every line of work doesn’t mean you don’t call on others for the products and services you need. You still get your haircut, see a doctor, talk to a lawyer, send your kids to school, etc.

Bottom Line

You initially believed that using an agent made sense. It probably still does.

Monday, January 25, 2016

Foreclosure Inventory Drops as Economy Improves

![Foreclosure Inventory Drops As Economy Improves [INFOGRAPHIC] | Keeping Current Matters](https://lh3.googleusercontent.com/blogger_img_proxy/AEn0k_uhzVcusnBhGKdaOh-t0MKwB9caGsC_iCkqz8V9cy6n9BfiVa70k3PXgRGB7SK497kfwlxJk9lMowUeMAVcPmua71lPHCM7bK0Gx3YhrWIsnrp_zRRQHZsCSjUb0OIOFI5PnBsGDSBrB7F2rWkKFC_3D9nFNYYyZ969K8arL-XSEQ=s0-d)

Some Highlights:

- Foreclosure Inventory has dropped year-over-year for the last 4 years (48 months).

- Only 3.4% of US homes are in serious delinquency.

- 29 states have a foreclosure inventory rate lower than the national average.

Sunday, January 24, 2016

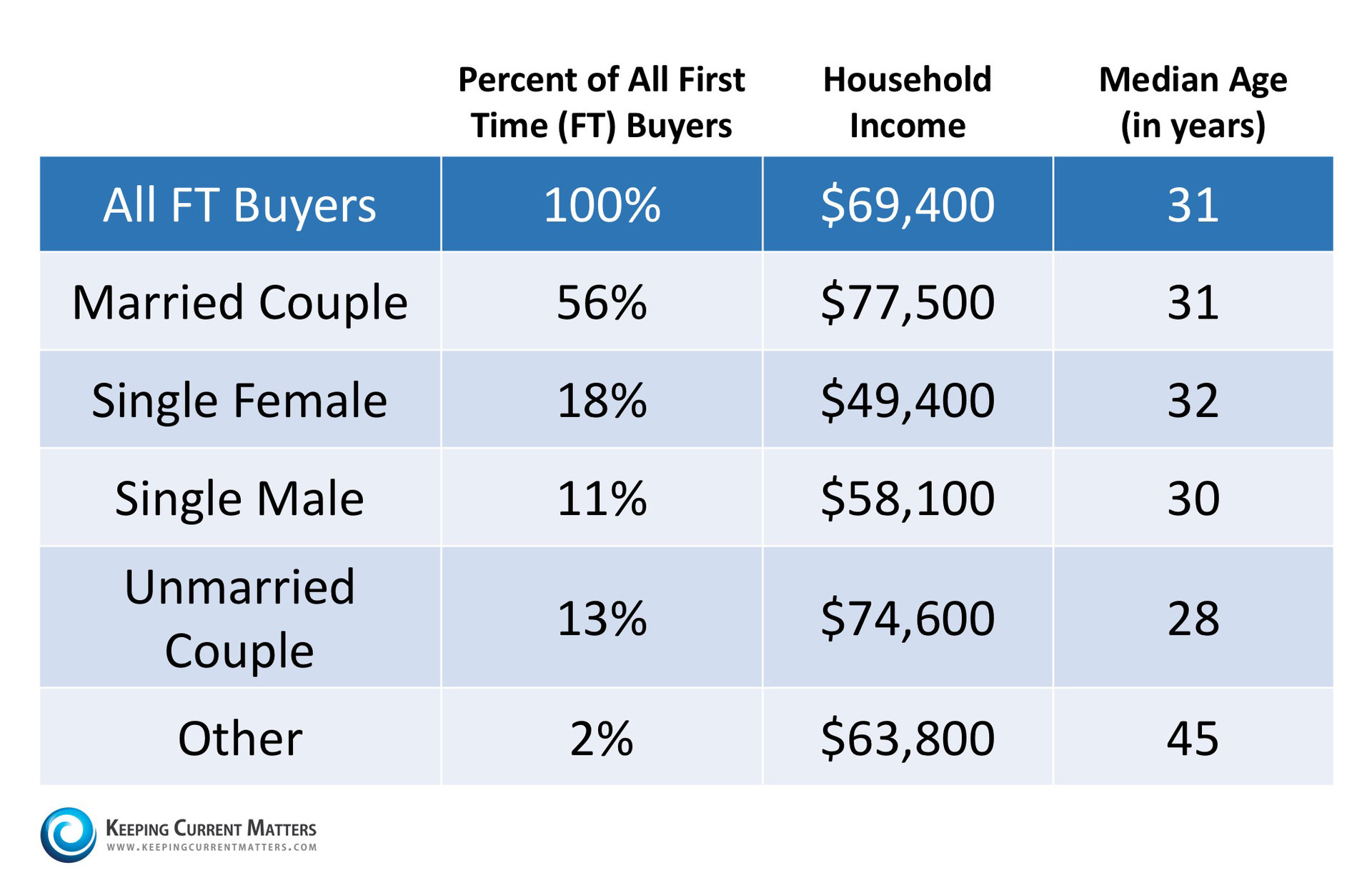

Are You Wondering What It Takes To Buy Your First Home?

There are many people sitting on the sidelines trying to decide if they should purchase a home or sign a rental lease. Some might wonder if it makes sense to purchase a house before they are married and have a family. Others may think they are too young. And still others might think their current income would never enable them to qualify for a mortgage.

We want to share what the typical first time homebuyer actually looks like based on theNational Association of REALTORS most recent Profile of Home Buyers & Sellers. Here are some interesting revelations on the first time buyer:

Bottom Line

You may not be much different than many people who have already purchased their first home. Meet with a local real estate professional today who can help determine if your dream home is within your grasp.

Saturday, January 23, 2016

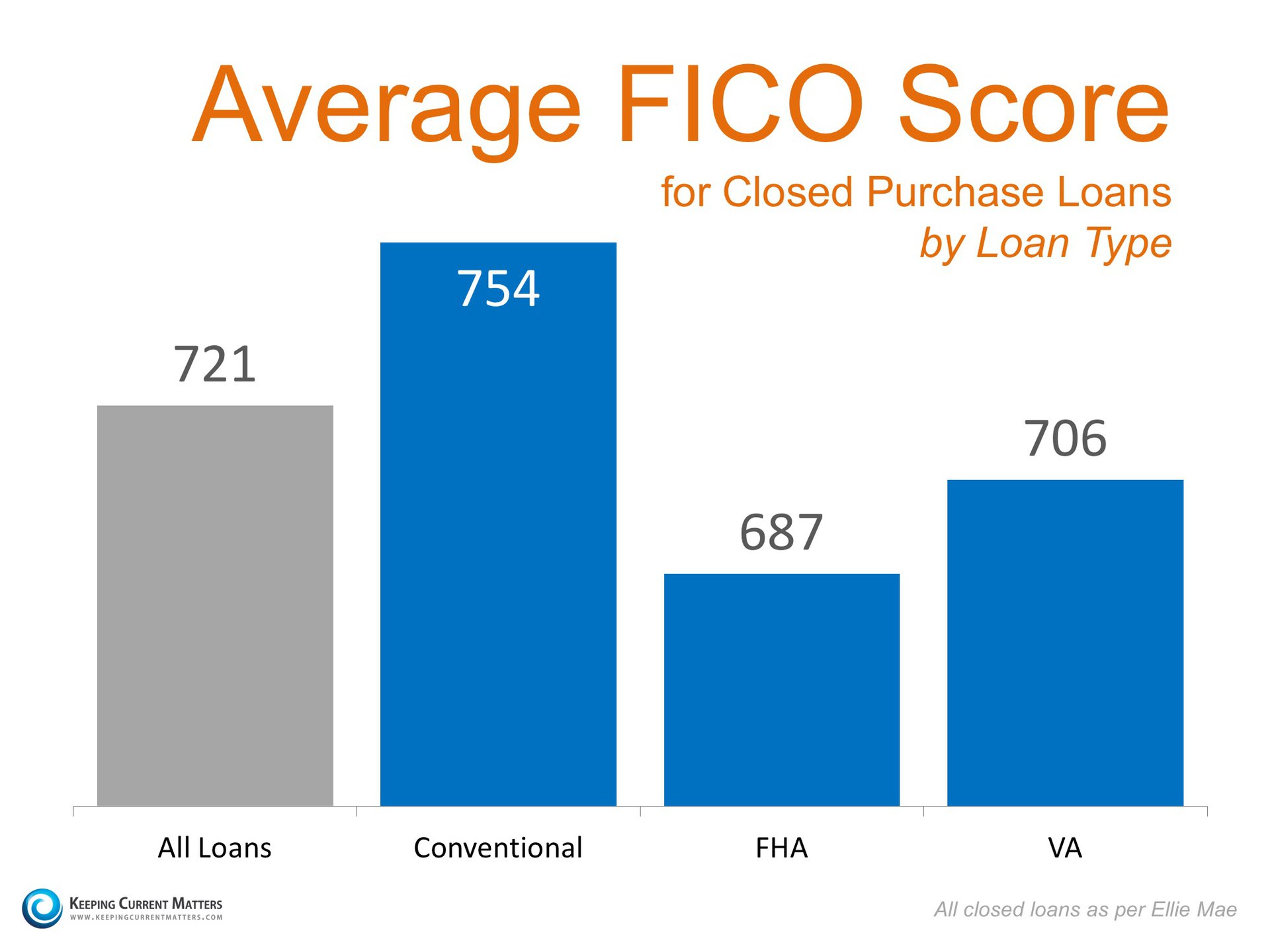

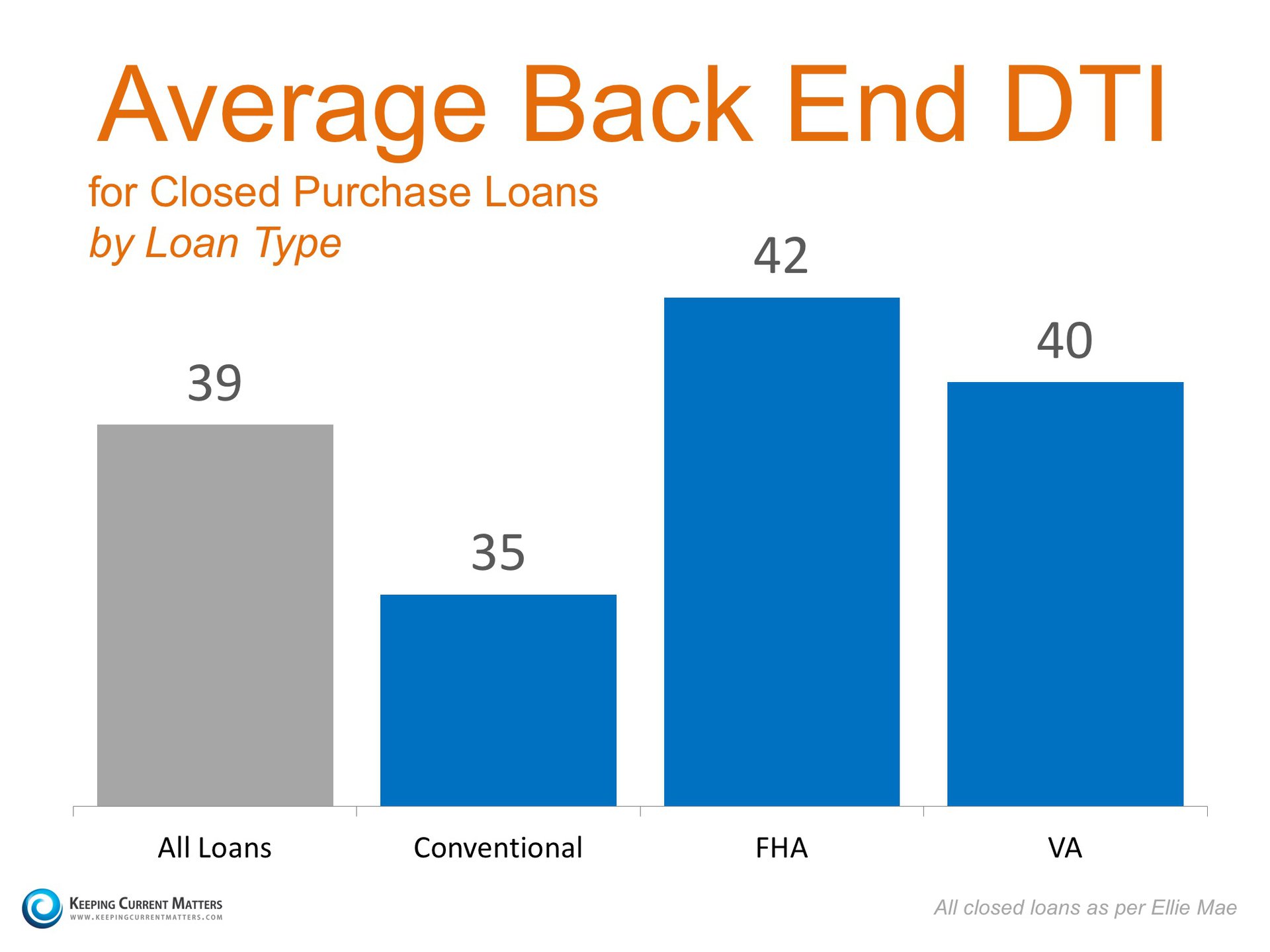

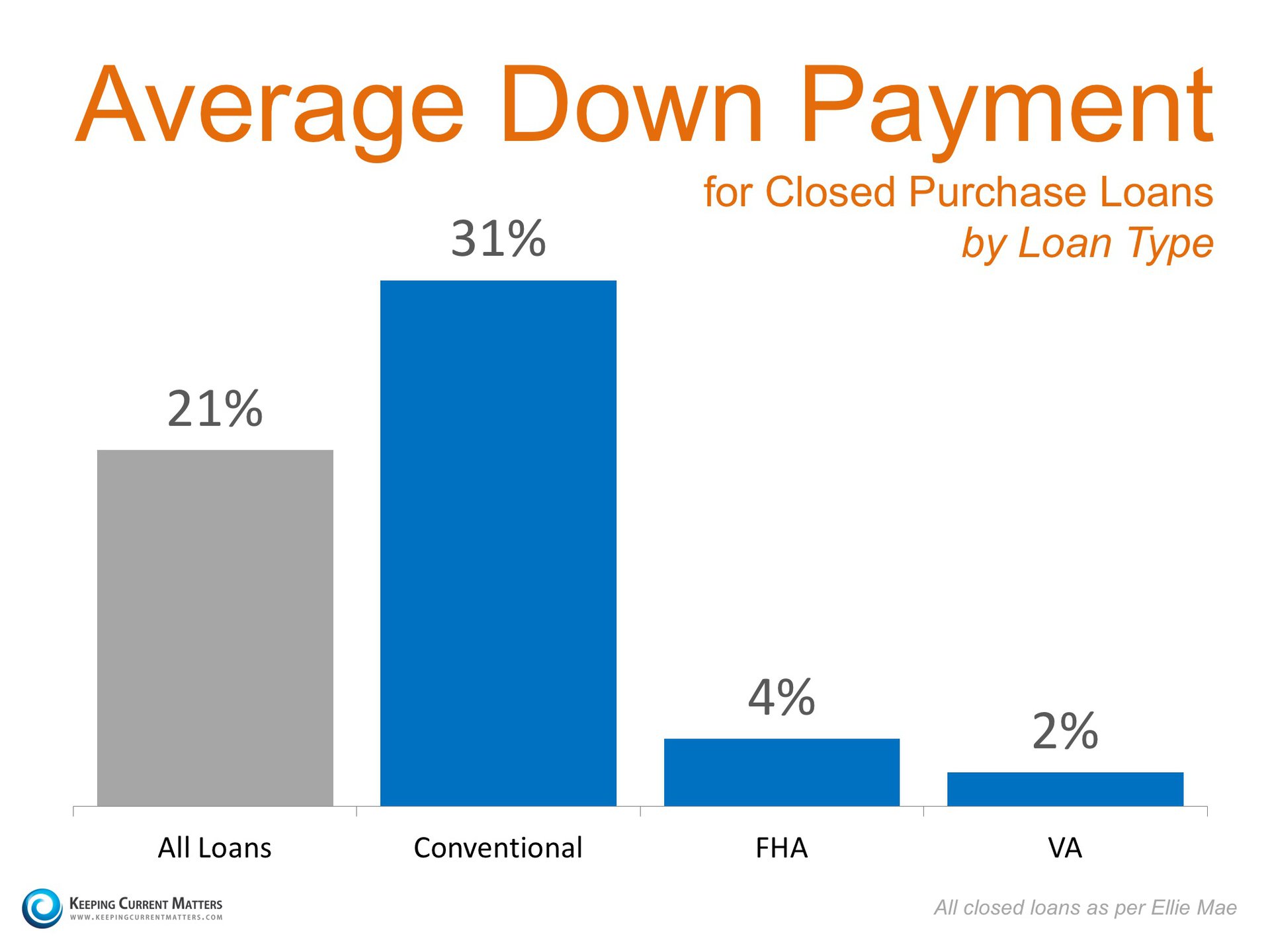

What Do You Actually Need to Get a Mortgage?

Fannie Mae recently released their “What do consumers know about the Mortgage Qualification Criteria?” Study. The study revealed that Americans are misinformed about what is required to qualify for a mortgage when purchasing a home. Here are three takeaways:

- 59% of Americans either don’t know (54%) or are misinformed (5%) about what FICO score is necessary

- 86% of Americans either don’t know (59%) or are misinformed (25%) about what an appropriate Back End Debt-to-Income (DTI) ratios is

- 76% of Americans either don’t know (40%) or are misinformed (36%) about the minimum down payment required

To help correct these misunderstandings, let’s take a look at the latest Ellie Mae Origination Insight Report, which focuses on recently closed (approved) loans.

FICO SCORES

BACK END DTI

DOWN PAYMENTS

Bottom Line

Whether buying your first home or moving up to your dream home, knowing your options will definitely make the mortgage process easier. Your dream home may already be within your reach.

Friday, January 22, 2016

Should I Buy Now a House Now Or Wait Until Next Year?

![Should I Buy Now Or Wait Until Next Year? [INFOGRAPHIC] | Keeping Current Matters](https://lh3.googleusercontent.com/blogger_img_proxy/AEn0k_t4O7Pp_BB9azX004uZ5ONlTRstY7OiQWsGQ4qYyWzSdEpjAaH12H_2XqiOGV5PE8BlbWEnk6E8mCMrjvMByf9CT4nNLEePWmhFrMqVRjDjAF650Se4yWSxGFk5IVNsRcF5U4Xau3VBOmLQyufotBKin9hlgxVqhyMs=s0-d)

Some Highlights:

- The Cost of Waiting to Buy is defined as the additional funds it would take to buy a home if prices & interest rates were to increase over a period of time.

- Freddie Mac predicts interest rates to rise to 4.8% by next year.

- CoreLogic predicts home prices to appreciate by 5.3% over the next 12 months.

- If you are ready and willing to buy your dream home, find out if you are able to!

Sunday, January 10, 2016

![Do I Need Perfect Credit to Buy a Home? [INFOGRAPHIC] | Simplifying The Market](https://lh3.googleusercontent.com/blogger_img_proxy/AEn0k_sKnVVQtjj2bawVhW4ulGN7yiZuRsz_kPcWiOXOtsLrU3TVO0vC28bptH8QoG45-21KJlcgFWeKwXUpEDCIZj98y5WMJMHU-seSwLpdkwwvn6Jc6NPvvPAOWnYbZoEIQDXDj_yjrgyVOPDmPjqU-2j_=s0-d)

Saturday, January 9, 2016

Foreclosure Listings

Friday, January 8, 2016

Don’t Let Rising Rents Trap You!

Don’t Let Rising Rents Trap You!

There are many benefits to homeownership. One of the top ones is being able to protect yourself from rising rents and lock in your housing cost for the life of your mortgage.

Don’t Become Trapped

Jonathan Smoke, Chief Economist at realtor.com recently reported on what he calls a “Rental Affordability Crisis”. He warns that,

“Low rental vacancies and a lack of new rental construction are pushing up rents, and we expect that they’ll outpace home price appreciation in the year ahead.”

The Joint Center for Housing Studies at Harvard University recently released their 2015 Report on Rental Housing, in which they reported that 49% of rental households are cost-burdened, meaning they spend more than 30% of their income on housing. These households struggle to save for a rainy day and pay other bills, such as food and healthcare.

It’s Cheaper to Buy Than Rent

In Smoke’s article, he went on to say,

“Housing is central to the health and well-being of our country and our local communities. In addition, this (rental affordability) crisis threatens the future value of owned housing, as the burdensome level of rents will trap more aspiring owners into a vicious financial cycle in which they cannot save and build a solid credit record to eventually buy a home.”“While more than 85% of markets have burdensome rents today, it’s perplexing that in more than 75% of the counties across the country, it is actually cheaper to buy than rent a home. So why aren’t those unhappy renters choosing to buy?”

Know Your Options

Perhaps, you have already saved enough to buy your first home. HousingWire reported that analysts at Nomura believe:

“It’s not that Millennials and other potential homebuyers aren’t qualified in terms of their credit scores or in how much they have saved for their down payment.It’s that they think they’re not qualified or they think that they don’t have a big enough down payment.” (emphasis added)

Many first-time homebuyers who believe that they need a large down payment may be holding themselves back from their dream home. As we reported last week, in many areas of the country, a first-time home buyer can save for a 3% down payment in less than two years. You may have already saved enough!

Bottom Line

Don’t get caught in the trap so many renters are currently in. If you are ready and willing to buy a home, find out if you are able. Have a professional help you determine if you are eligible to get a mortgage.

Thursday, January 7, 2016

Thinking of Selling Your Home? Get Ready to Negotiate!

Thinking of Selling Your Home? Get Ready to Negotiate!

Now that the market has showed signs of recovery, some sellers may be tempted to try and sell their home on their own (FSBO) without using the services of a real estate professional.

Real estate agents are trained and experienced in negotiation. In most cases, the seller is not. The seller must realize their ability to negotiate will determine whether they can get the best deal for themselves and their family.

Here is a list of some of the people with whom the seller must be prepared to negotiate if they decide to FSBO:

- The buyer who wants the best deal possible

- The buyer’s agent who solely represents the best interest of the buyer

- The buyer’s attorney (in some parts of the country)

- The home inspection companies, which work for the buyer and will almost always find some problems with the house.

- The termite company if there are challenges

- The buyer’s lender if the structure of the mortgage requires the sellers’ participation

- The appraiser if there is a question of value

- The title company if there are challenges with certificates of occupancy (CO) or other permits

- The town or municipality if you need to get the COs permits mentioned above

- The buyer’s buyer in case there are challenges on the house your buyer is selling

- Your bank in the case of a short sale

Bottom Line

The percentage of sellers who have hired a real estate agent to sell their home has increased steadily over the last 20 years. Let's get together and discuss all we can do to make the process easier for you.

Wednesday, January 6, 2016

W3315 Ranch Rd Watertown, Wisconsin 53094

W3315 Ranch Rd Watertown, Wisconsin 53094

Lower Unit 2 Bedroom 1 Bath

Upper Unit 1 Bedroom 1 Bath

List Price: $179,900

Contact Heidi Buchberger RE/MAX Realty Center for information on Concord, Sullivan, Watertown, & Farmington Properties For Sale!

Tuesday, January 5, 2016

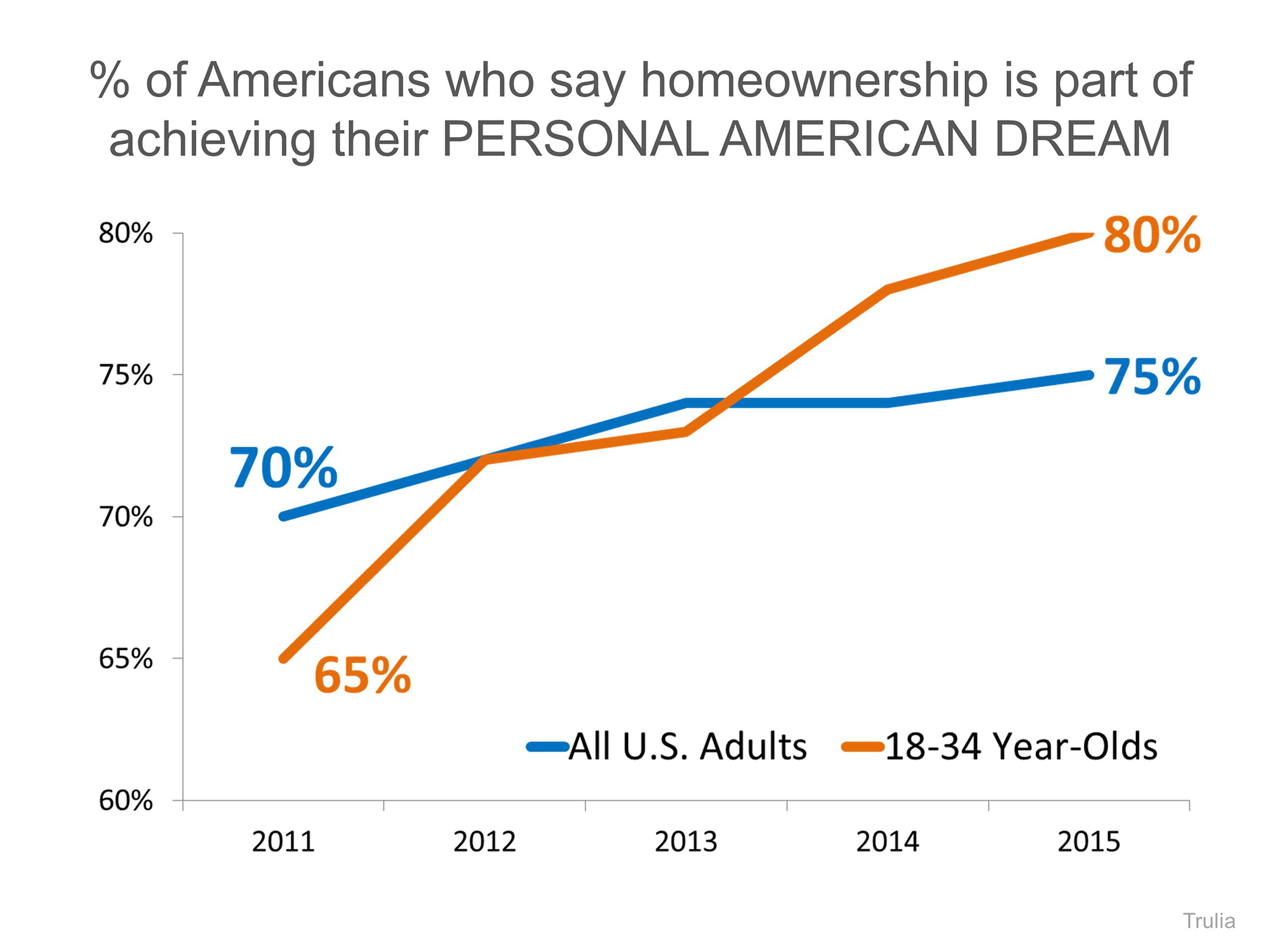

American Dream of Homeownership Still Very Much Alive

American Dream of Homeownership Still Very Much Alive

In a recent post, Trulia examined whether homeownership was again being seen by adults in the US as a “part of their personal American Dream.” Over the last five years:

- The percentage of U.S. adults who believe homeownership is part of their American Dream increased from 70% to 75%

- The percentage of 18-34 Year-olds who believe homeownership is part of their American Dream increased from 65% to 80%

Here is a graph of the survey over the last five years:

Bottom Line

As the housing industry recovers from the crisis of 2008-2010, Americans belief in homeownership as part of their own personal American Dream has also made a strong comeback.

FREE CMA- January

The weather may be a bit chilly, but now is the time to think about home SELLING!

Call Heidi 262-443-2672

Friday, January 1, 2016

Subscribe to:

Comments (Atom)